Ryman Hospitality Properties (RHP)·Q4 2025 Earnings Summary

Ryman Hospitality Posts Record Q4 Revenue, Raises 2026 Dividend to $4.80

February 24, 2026 · by Fintool AI Agent

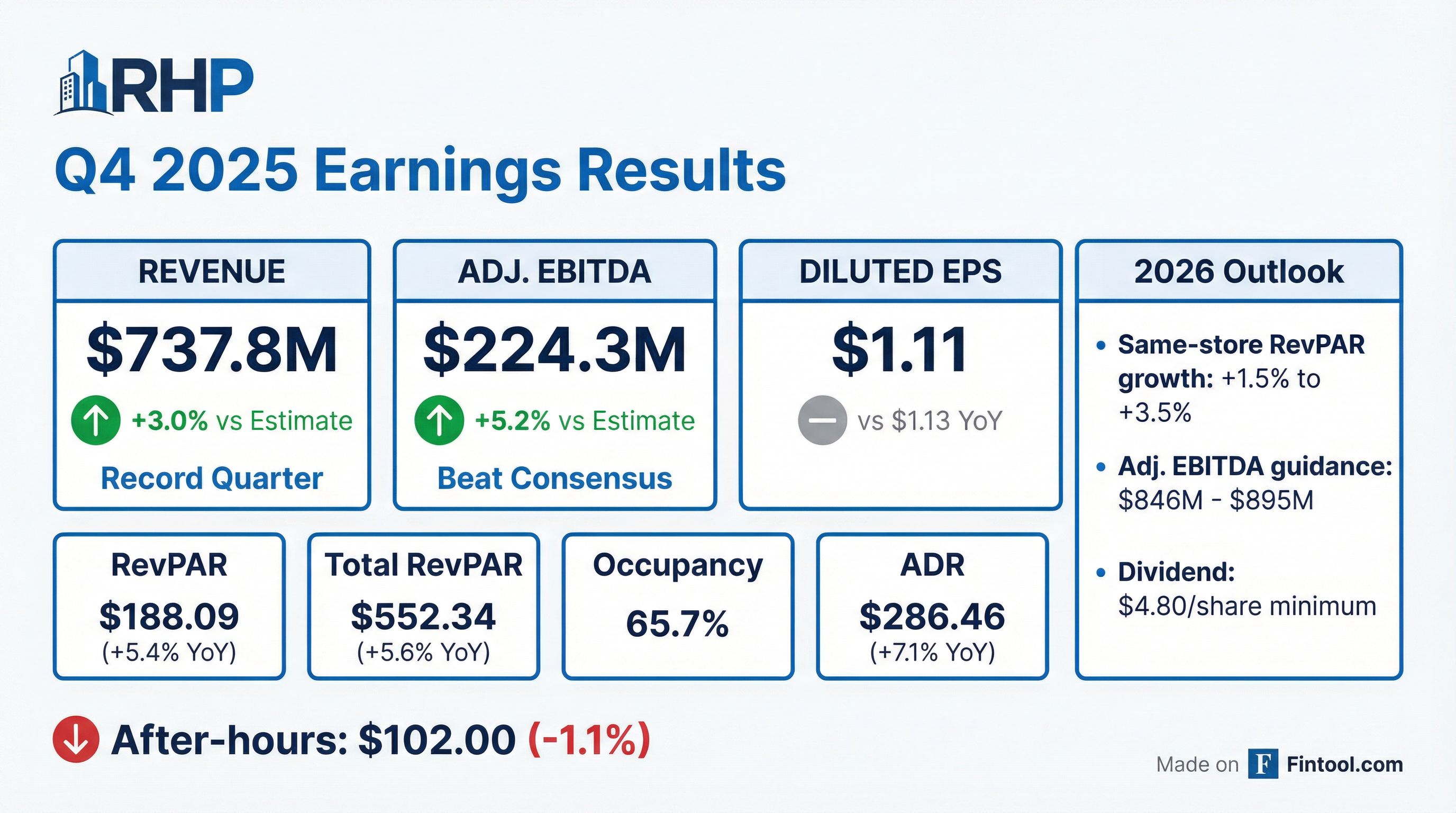

Ryman Hospitality Properties (NYSE: RHP) reported Q4 2025 results that topped estimates across key metrics, delivering all-time record quarterly revenue of $737.8 million driven by strong holiday programming at its Gaylord Hotels and robust demand at its Nashville entertainment venues.

The lodging REIT, which owns five of the top seven largest non-gaming convention center hotels in the U.S., beat revenue estimates by 3.0% and Adjusted EBITDAre estimates by 5.2%. Management provided 2026 guidance projecting low single-digit same-store Hospitality growth and announced a dividend increase to $4.80 per share minimum for the year. On the earnings call, Executive Chairman Colin Reed highlighted that the company's stock has generated 12.5% annualized returns since the 2012 REIT conversion—2.5x its next closest peer.

Did Ryman Beat Earnings?

Revenue and EBITDA beat consensus, while EPS declined on higher share count.

The EPS decline reflects the impact of approximately 3.0 million additional shares issued in May 2025, which increased diluted share count to 67.6 million from 63.7 million in the prior year period. On a per-share basis, Adjusted FFO—the more relevant metric for REITs—increased 10.7% YoY.

Ryman has now beaten revenue estimates in 6 of the last 8 quarters, demonstrating consistent execution despite macroeconomic headwinds.

What Drove the Record Quarter?

Holiday programming, ADR growth, and the Desert Ridge acquisition fueled outperformance.

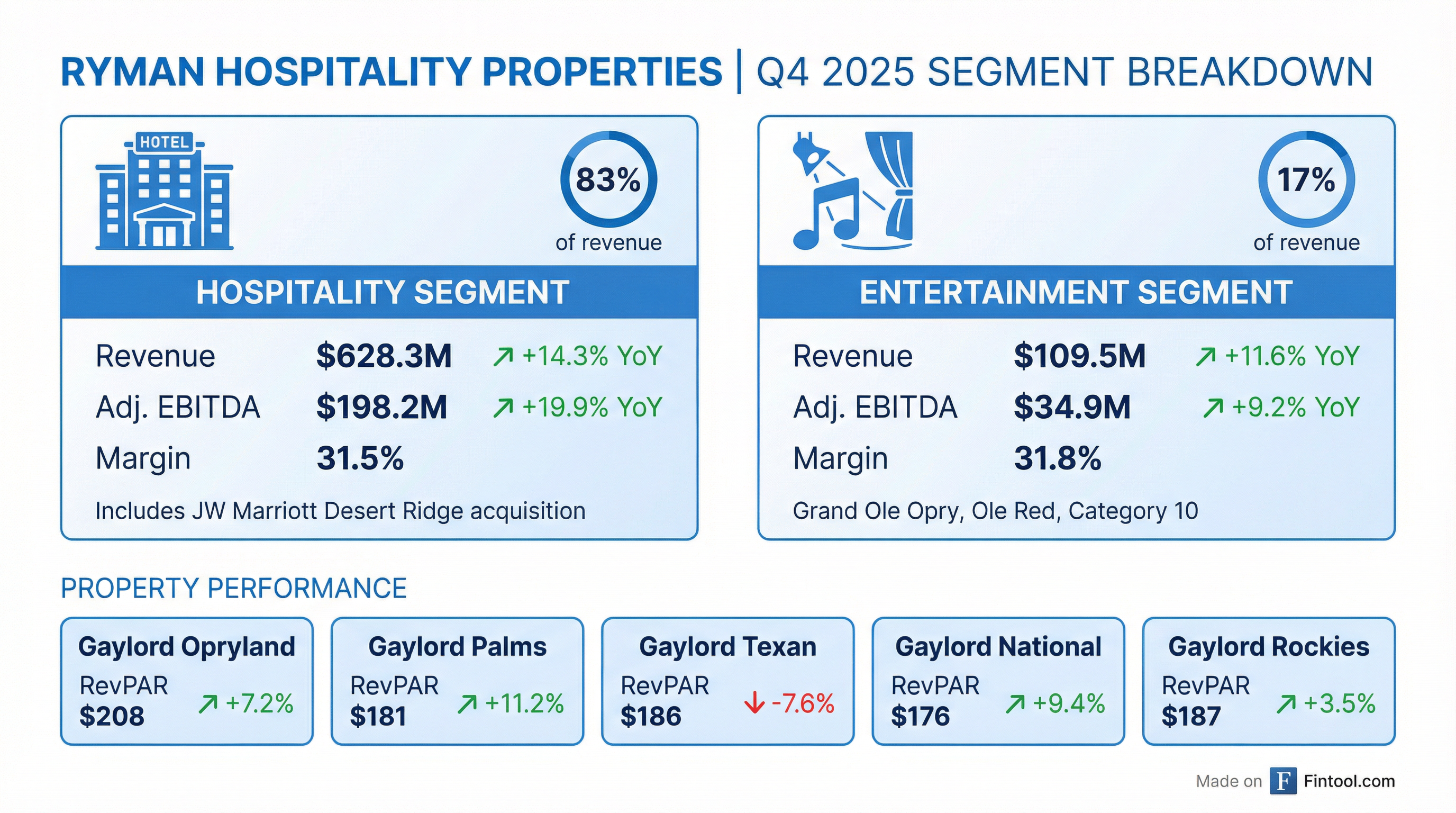

The Hospitality segment delivered revenue of $628.3 million, up 14.3% YoY, driven by:

-

ICE! holiday programming success: Over 1.5 million ticketed guests, up 14.2% YoY, with record attendance at Gaylord Opryland and Gaylord Rockies. Gaylord National had its best ICE! season since 2010, and the JW Hill Country achieved the highest guest satisfaction ratings across the portfolio.

-

Strong ADR growth: Same-store ADR increased 5.1% to $280.98, with new bookings for future periods at record $299 ADR (+6.1% vs prior year)

-

JW Marriott Desert Ridge contribution: The June 2025 acquisition added $50.1 million in Q4 revenue with 28.9% Adjusted EBITDAre margin

The Entertainment segment posted record Q4 revenue of $109.5 million (+11.6% YoY), driven by stronger volumes at downtown Nashville venues and record October performance at the Grand Ole Opry during its birthday month. The Opry 100 centennial programming delivered all-time high monthly revenue and EBITDA for the brand.

How Did Individual Properties Perform?

RevPAR was mixed across properties, with Palms and National outperforming while Texan lagged.

Gaylord Texan underperformance: RevPAR declined 7.6% due to ongoing rooms renovation that began in July 2025 and is expected to complete by mid-2026. Occupancy dropped 7.6 percentage points to 67.1%.

Gaylord Palms outperformance: RevPAR surged 11.2% as occupancy increased 3.5 percentage points to 63.8%, benefiting from strong leisure demand and ICE! programming.

What Did Management Guide?

2026 guidance implies low single-digit same-store growth with meaningful contribution from Desert Ridge.

CEO Mark Fioravanti noted that projected same-store group rooms revenue on the books for 2026 is pacing 6.0% above the same time last year, with projected ADR on the books approximately 4.6% higher. The gap between 6% group pace and 2.5% RevPAR guidance reflects conservative assumptions for in-year bookings, attrition, cancellations, and leisure performance.

Conservative stance: Management cited "political and geopolitical issues that are occurring right now in the economy" as the reason for the measured outlook. Q1 2026 is expected to show flat RevPAR and entertainment EBITDA down several million dollars vs. a tough Q1 2025 comparison.

Winter Storm Fern impact: Guidance includes estimated business impact from Winter Storm Fern, which disrupted January results. "We were pacing ahead as we started January until we got to that winter storm."

What Changed From Last Quarter?

Group booking momentum accelerated, meeting planner sentiment improved, and capital allocation expanded.

Record December bookings: December was "the very best December production, in terms of room nights, that we've ever seen in the company's history," according to COO Patrick Chaffin. Meeting planner sentiment improved significantly as tariff-related hesitancy from Q3 eased.

RevPAR index at all-time highs: Same-store portfolio achieved 143% RevPAR index vs Marriott comp set in Q4, up 1,200 basis points YoY. Full-year RevPAR index of 127% was up 610 basis points YoY.

Credit facility refinancing: In January 2026, RHP refinanced its corporate revolving credit facility, increasing capacity from $700M to $850M and extending maturity from May 2027 to January 2030.

Fitch upgrade: In December, Fitch upgraded the corporate family rating to "BB" from "BB-", triggering a 25 basis point spread reduction on the Term Loan B.

Entertainment expansion: Post quarter-end, OEG announced:

- Third Category 10 venue at Universal CityWalk Orlando, adjacent to Islands of Adventure, opening late 2027

- Category 10 Las Vegas opening Q4 2026

- CCNB Amphitheatre management contract in Simpsonville, SC

What Did Analysts Ask About?

Q&A focused on group booking trends, Rockies expansion, and competitive positioning.

On group business mix: Corporate mix is 3 percentage points higher than last year, positioning the company well for higher outside-the-room spend. Government business represents just 0.4% of bookings on the books—"we have been pivoting away from it."

On Gaylord Rockies expansion: Executive Chairman Colin Reed said the company is "a lot nearer pulling the trigger on an expansion in that hotel today than we were a year ago." The property has highest occupancy and strongest group demand ever. Management expects more detail in the next 1-2 quarters.

On rate trajectory: ADR on the books for 2028 and beyond is up over 5%, maintaining mid-single-digit rate growth. "Rate is more sticky. It's going to stay with us once it's booked."

On AI impact: CEO Mark Fioravanti noted that hospitality and live entertainment are "almost kind of an anti-AI play" because "people are gonna value being face-to-face with other human beings in the same room." The company is focused on AI applications in sales transactions, revenue management, and labor scheduling.

On Opryland earnings power: Reed stated this year "that hotel will push $200 million of EBITDA out of it. There is not another hotel like this in America." The new Foundry Fieldhouse sports bar is designed to capture unmet food and beverage demand.

On JW cross-selling success: The company booked 22,000 multi-year room nights through JW Marriott rotational sales synergies after integrating Desert Ridge and Hill Country sales teams.

How Did the Stock React?

Stock traded down 1.1% in after-hours despite the beats.

RHP closed at $103.11 on February 23, 2026, down 1.9% on the session. In after-hours trading following the earnings release, shares dipped to $102.00, down approximately 1.1% from the close.

The muted reaction likely reflects:

- Gaylord Texan weakness: The property's 7.6% RevPAR decline and ongoing renovation disruption

- Conservative 2026 outlook: Same-store RevPAR guidance of +1.5-3.5% implies deceleration from 2025's +3.1%

- Share dilution: Diluted EPS declined YoY despite strong operating results

Year-to-date, RHP is up approximately 8.7% vs the S&P 500's 4.3% gain.

What Are the Key Risks and Catalysts?

Capital expenditure cycle creates near-term noise but positions portfolio for long-term growth.

2026 Catalysts:

- Foundry Fieldhouse opening (April 2026): Sports bar, pavilion, and event lawn at Gaylord Opryland

- Category 10 Las Vegas (late 2026): Expands entertainment platform to new market

- Gaylord Texan renovation completion (mid-2026): Should remove RevPAR headwind

- Opry 100 celebration: Centennial programming expected to drive Entertainment segment growth

Key Risks:

- Macroeconomic sensitivity: Group travel and convention demand correlate with corporate confidence

- Geographic concentration: Heavy Nashville exposure (~40% of entertainment revenue)

- Renovation disruption: JW Marriott Hill Country rooms renovation begins April 2026 ($90M project)

- Leverage: Total debt of $4.0B with Net Debt/EBITDA around 4.7x

Balance Sheet Update

The debt increase reflects the JW Marriott Desert Ridge acquisition and ongoing capital investments. Management estimates 2025 construction disruption impacted same-store RevPAR by approximately 190 basis points.

Management Tone and Outlook

Executive Chairman Colin Reed struck a confident tone, emphasizing the company's competitive moat and long-term positioning:

"Since our REIT conversion announcement in 2012, our stock has generated a nearly 12.5% annualized return, including reinvested dividends. This represents a rate of return of approximately 2.5x greater than that of our next highest REIT peer over the same period."

On the entertainment business, Reed was particularly bullish: "Live entertainment is such a sought-after commodity in this day and age. I think we see a lot of growth in this business over the next 3, 4, 5 years... we spend more of our time fielding inbound opportunities on this business than we do certainly on our hotel business."

Regarding macroeconomic uncertainty, CEO Fioravanti acknowledged that guidance reflects "a fairly conservative view on demand for the year" given "political and geopolitical issues that are occurring right now in the economy." However, management emphasized that "the early indicators that we look for, we're not seeing anything flashing yellow or flashing red."

The Bottom Line

Ryman delivered a strong Q4 with record revenue and EBITDA beats, demonstrating the resilience of its group-oriented hotel model and growing entertainment platform. The 2026 outlook is constructive but conservative, with same-store growth expected to moderate as renovation disruption continues.

The earnings call revealed several positive developments not in the press release: record December bookings, Rockies expansion moving closer to approval, and 143% RevPAR index vs. competitors. Management's confidence in the live entertainment segment and JW integration success provide catalysts beyond core hospitality.

The stock's muted reaction suggests investors are focused on the Gaylord Texan headwind and decelerating growth trajectory rather than the fundamental strength. At current levels (~$102), RHP trades at approximately 11.7x 2026 Adjusted FFO guidance ($8.75 midpoint) and offers a 4.7% dividend yield—attractive relative to lodging REIT peers but reflecting execution risk around the multi-year capital deployment program.

Related Links: